Q 1 2014 Office and Industrial Market Report San Fernando Valley

Q1 2014

Market Moves a Tad Slower in Quarter, But Longer Term Trends Remain Positive

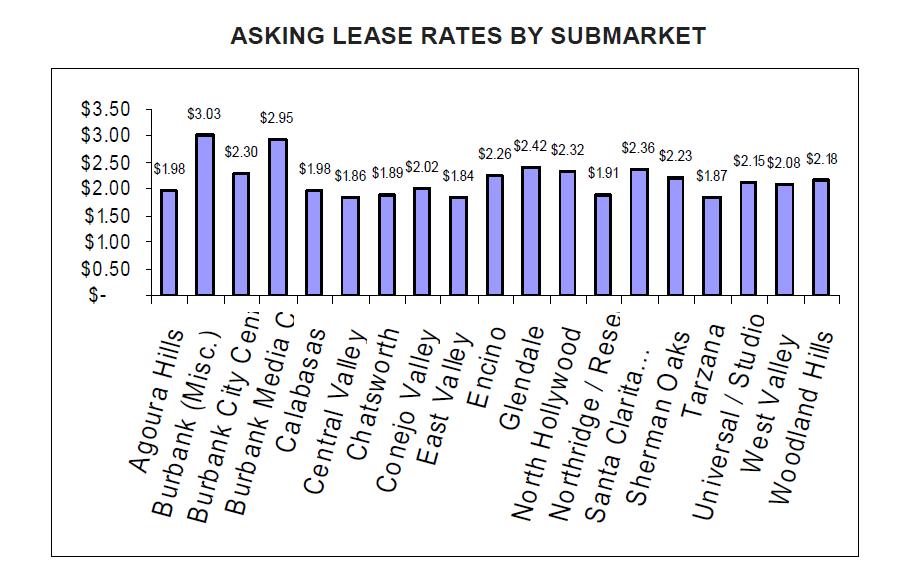

The Los Angeles North office market quieted down somewhat in the first quarter, although leasing activity continued to exceed 1 million SF.

Vacancy levels remained unchanged at 16.2 percent compared to the fourth quarter, and have fallen nearly 100 basis points (bps) compared to vacancies of 17.1 percent in the same period last year.

Just over 1 million SF of office space was leased in the quarter, about 38 percent less than the 1,624,000 SF leased in Q4 and down from the year ago period as well. The slowdown in velocity seems to have impacted absorption during the quarter, but it’s equally important to note that leasing has been strong now for the past nine quarters, an indication that the recovery in the office market is proceeding at a pace consistent with the economic growth we are seeing.

Only 31,200 SF of space was leased on a net basis during the quarter, down significantly from Q4 when net absorption totaled 298,035 SF. However, over the past 12 months, 504,000 SF of space has been leased on a net basis, amounting to a solid 1.1 percent growth in occupied space over that period.

With that level of progress, developers are reentering the market. Although the 200,000 SF of office space currently under construction is probably insufficient to make any real impact on available inventory, it is indicative of a return of confidence. Not to be overlooked, Laurel Canyon Plaza, a 90,000 square foot office building in North Hollywood and a neighboring retail building, was acquired by Goldstein Planting Investments for redevelopment.

Indeed, the Allen Matkins/UCLA Anderson Forecast Commercial Real Estate Survey released late in January showed that sentiment in the office market is highest in Southern California. About 70 percent of the survey respondents in the region said they planned to commence one or more projects within the next 12 months.

Sales activity too slowed in the quarter with just 10 sales taking place, compared with 19 in the year-ago period. With fewer transactions, the median price of office buildings sold declined to $205 PSF in Q1 from $257 PSF in Q4 and $212 PSF in Q1, 2013. Still, several trophy properties changed hands including Tower Burbank and Westlake Park Place.

Industrial Absorption Rises to Pre-Recession Levels and Vacancies Fall Below 4 Percent

Following four quarters of robust leasing activity, absorption has risen to pre-recession levels and vacancy has fallen to the lowest levels the market has seen since 2009.

With little new construction and a resurgence of demand for industrial space, the upward trajectory of the Los Angeles North industrial market seems here to stay, at least for the time being.

Some 1,100,404 SF of industrial space was leased in the quarter, bringing vacancy levels down to 3.8 percent, the first time vacancies have fallen below 4 percent since the fourth quarter of 2009. Current vacancy levels have fallen 40 basis points (bps) compared with the prior quarter and year ago period, which both registered vacancies of 4.2 percent.

Not surprisingly, leasing velocity has slowed somewhat from the prior quarter when 1,475,538 SF of space was leased, as well as the year ago period when 1,824,794 SF was leased as options for businesses become extremely constrained. Eight of the 13 Los Angeles North submarkets now are operating with vacancy levels below 3 percent. In the North Hollywood/Universal City submarket, vacancy is 0.9 percent. In Northridge it is 1.2 percent and in Reseda/Tarzana it is 1.5 percent. Only the Antelope and Santa Clarita valleys show vacancy rates above 5 percent.

On a net basis, some 625,600 SF of industrial space was leased, more than in any quarter since the first quarter of 2006 when 645,688 SF of space was absorbed. Admittedly, we are still seeing some fluctuation in absorption rates, and negative 135,923 SF was registered in Q4, but given the solid leasing activity, the volatility is more likely due to the lapsed time between space leased and occupied.

Similarly the sales sector was more active than it has been in any first quarter since 2009 with 23 industrial buildings changing hands in the quarter. The median sale price rose 19 percent to $130 per square foot, compared with $109 per square foot in Q4.

Although there are still some distressed assets being cleared in the region, their numbers are minimal. In the current quarter, just two distressed properties changed hands, compared to six in the first quarter of 2013.

EricNishimoto-RE

EricNishimoto-RE